Related

EU Omnibus Packages Part 5: Omnibus V – Simplifying EU Defense Regulation

EU Omnibus Packages Part 4: Omnibus IV — Product Regulation, Simplification, and Compliance

Athletes Disqualified at 2026 Winter Olympics Over PFAS

EU Omnibus Packages Part 3: Simplifying EU Agricultural Regulation

In 2025, the Asia-Pacific (APAC) region is expected to see a significant evolution in its chemical management frameworks, including the adoption of the Globally Harmonized System (GHS), expanding control of per- and polyfluoroalkyl substances (PFAS), and increasingly stringent regulations modeled after the EU's Registration, Evaluation, Authorization, and Restriction of Chemicals (REACH) system, among others.

“These changes reflect a global trend to improve chemical safety and protect human health and the environment,” said Chanyanis Utiskul, regulatory research analyst at 3E.

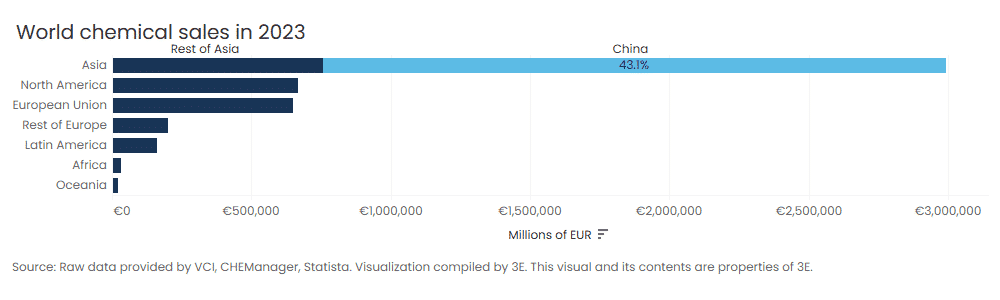

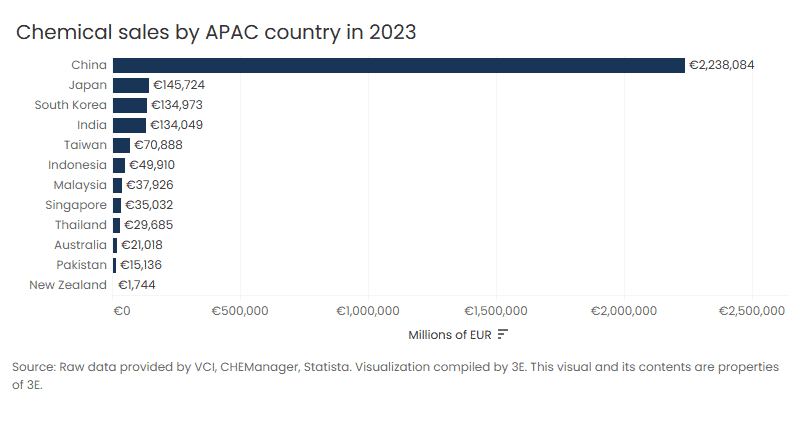

The APAC region is leading the world in chemical production, with most recent data showing combined countries selling nearly €3 trillion of chemicals in 2023. As nations in the region adopt more stringent measures, the focus on hazardous chemicals is intensifying, with a notable shift toward banning or restricting substances that pose significant risk. This proactive stance not only aligns with global trends toward enhanced chemical safety but also positions APAC nations as pivotal players in the international regulatory landscape.

China's Macroeconomic Environment and Influence

Before we discuss APAC's forecasted regulatory landscape, it is important to note China's macroeconomic conditions and chemical industry influence over Asia-Pacific and global industries.

While China's chemical industry is a commanding force on the global chemical stage, the country's economic standing has impacted both China’s domestic chemical industry and the global chemical industry as a whole. Specifically, China's ongoing housing crisis and weak domestic demand have placed significant hardship on Chinese industry. Meanwhile, China is still producing high volumes of basic chemicals with a mismatched demand, leading to overcapacity issues.

Dr. Kai Pflug, CEO of Management Consulting – Chemicals Ltd., based in Shanghai, said that if the current economic slowdown in China persists, particularly in construction, the growing chemical capacity cannot be utilized for domestic consumption and industry will instead seek export markets.

“Generally speaking, the weaker the Chinese economy is, the more pressure there will be on global chemical prices and the global chemical industry,” Pflug told 3E in an interview.

Pflug identified three areas that chemical companies should focus on regarding China in 2025:

- Chinese GDP growth, particularly in construction, as a revitalization of this segment could significantly improve domestic demand and decrease overcapacity issues.

- Trade war with the U.S., as the promise of high tariffs on chemicals from China imposed by the U.S. will “force Chinese exporters to target alternative markets more aggressively, potentially driving down global prices,” according to Pflug.

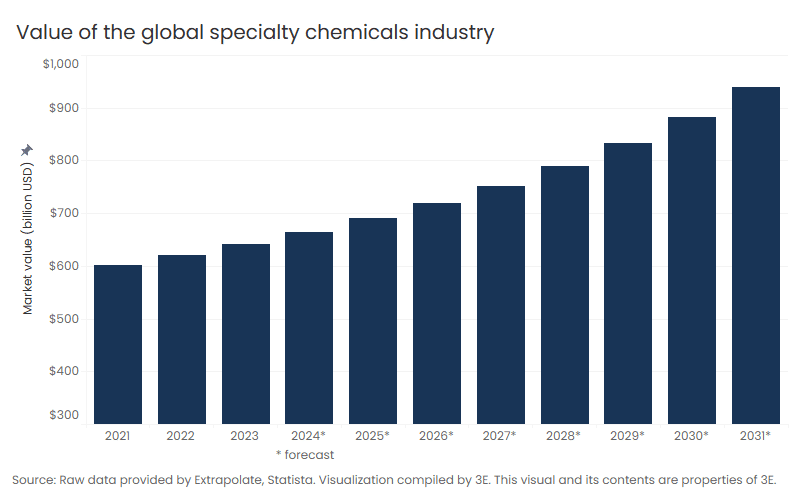

- Shift to specialty chemicals, as companies will be forced to move into specialties to increase profitability and stay competitive with chemical companies globally. Specialty chemicals, used in semiconductors and electronic vehicles, are becoming more and more in demand as the world migrates to high-tech developments.

Chemical Management Frameworks

In 2025, APAC countries are expected to expand or change their chemical management frameworks. Forecasts indicate some frameworks will be stricter in controlling hazardous substances by way of casting a wider net of hazardous categorization and tightening the reins on hazardous substances applications. Other reforms have been introduced to simplify chemical regulations, providing businesses with more flexibility in meeting their compliance obligations under the new chemical notification processes.

Utiskul said regulatory frameworks are being updated in certain APAC countries to enhance control over high-risk chemicals - namely PFAS, chemical weapons, and mercury - to meet obligations of the Stockholm, Rotterdam, Minamata, and Chemical Weapons Conventions, adding more obligations to businesses. The countries expected to tighten controls include:

- Thailand is modernizing its Hazardous Substances Act and regulations to align with trading partners and international standards, including implementing stricter licensing standards for PFAS. Meanwhile, regulations regarding exemptions from compliance are also becoming more stringent, and businesses must provide additional documentation as part of the exemption criteria.

- Vietnam is on track to finalize the Law on Chemicals in mid-2025, which will implement stricter regulations for managing chemical products throughout their life cycles, potentially expanding to a broader range of businesses, especially those dealing with high-risk chemicals, including those regulated by international agreements and conventions.

- China issued a new draft of its Restriction of Hazardous Substances (RoHS), making previously recommended national standards mandatory in late 2024, which is expected to go into effect in 2025. In this new standard, China will restrict 10 harmful substances in electrical and electronic equipment.

- New Zealand is also enhancing control of hazardous substances by introducing chemical annual report duties.

- Australia's Industrial Chemicals Introduction Scheme (AICIS) has revised the new chemical notification process in a significant move to facilitate business compliance. This update simplifies the record-keeping and reporting requirements in line with the revised Australian Industrial Chemicals (General) Rules 2019 and the Industrial Chemicals Categorization Guidelines.

Similarly, the Philippines and Malaysia are on track to simplify their chemical regulations in 2025 to ease the reporting burden on businesses. In the Philippines, new guidelines have been proposed that would make the new chemicals notification process more straightforward for businesses by simplifying confidential business information data requirements, including provisions for intermediates, impurities, and chemical byproducts. Malaysia is also anticipating revising many guidelines in 2025 to help industries comply with regulations pertaining to chemicals used in the workplace that are hazardous to health.

“Businesses are facing increased regulatory scrutiny and obligations,” Utiskul said. “While some reforms are intended to reduce regulatory burdens, the new regulations will require companies to stay alert and be prepared to adapt to this evolving landscape.”

REACH-Like Developments

Some APAC countries model regulatory legislation after U.S. and EU regulatory standards, one of which is the EU REACH. In 2025, businesses can expect to see a continued development of REACH-like legislation in Asia-Pacific countries, notably India's potential adoption of REACH-like legislation and Korea's expansion of its REACH legislation.

In India, the latest Draft Indian Chemicals (Management and Safety) Rules (ICMSR) is awaiting finalization and would require a new framework for notification, registration, chemical safety assessments, restrictions, safety data sheets (SDS), and labeling. This represents a big overhaul in India's chemical management and includes many changes that correlate to volume produced or imported in the country. Fees will be applied for registration, notifications, requests for authorizations, restricted substances, and confidentiality requests based on a tonnage band of chemicals. Additionally, noncompliance fees will also be issued.

“This initiative seeks to enhance enforcement under the existing chemicals rules, ensuring that all chemicals circulated in the country are properly regulated,” Utiskul said of India's ICMSR draft.

Originally drafted in 2020, the legislation has been on hold, and ongoing delays have led to uncertainty as to when the rule will be implemented. Some expect that the government will submit the final draft to the World Trade Organization for comment before officially adopting it.

In Korea, K-REACH is projected to undergo changes in 2025. Starting in January 2025, the annual tonnage of manufactured to imported chemicals between 0.1 and 1 ton no longer requires registration, only notification, saving companies the compliance cost from the registration duty for new chemicals manufactured or imported annually. However, a hazards indication requirement was newly introduced by the Ministry of Environment into the notification process for new chemicals under 1 ton, which was not required under the previous K-REACH.

“While the Ministry of the Environment (MoE) stresses that the required hazard information should be easily accessible and it does not expect companies to generate hazard data at their own expense, this new requirement will impose additional administrative burdens and costs on the industry, particularly for small and medium-sized enterprises that previously did not need to obtain hazard data to carry out their notification duty,” said Kristyn Hong, associate director of regulatory research at 3E.

If the hazard information is not submitted for notification, the chemicals will be classified as “hazard pending,” meaning they will be considered potential hazards and subject to specific safety measures and additional compliance obligations.

Additionally, a more robust toxic categorization system will be implemented by K-REACH and the Chemicals Control Act (CCA) in August of 2025. The new categorization organizes chemicals based on their acute, chronic, and ecological hazardous threat. More specific subcategories may be added in early 2025.

Hong said that the regulatory update introduces differentiated inspection obligations for hazardous chemical substance handling facilities based on risk levels and quantity.

“Companies handling low-risk or chronic hazardous substances will have a reduced administrative burden as they are exempted from regular and installation inspections,” Hong said. “However, companies handling substances that fall under stricter categories (such as acute hazardous substances) may face increased compliance efforts due to the heightened controls on these materials.”

China and Japan are also expanding their REACH-like policies. China's New Pollutant Policy will require screening, assessing, and managing risks associated with new substances.

Japan has continued to expand its coverage of toxic substances under the Industrial Safety and Health Law (ISHL), which will add 1,497 substances in April 2025 and nearly 800 more in April 2026. By 2026, approximately 2,900 substances will have been added to the hazardous classification lists and will be subject to increased regulation, and additional expansions have been drafted for 2027 and 2028.

PFAS Control

Like the EU's REACH, the Stockholm Convention, a multilateral treaty, informs a lot of regulatory action in the Asia-Pacific region, specifically when it comes to PFAS control. Under the Stockholm Convention framework, PFAS are categorized as persistent organic pollutants (POPs) and are increasingly subjected to restrictions and prohibitions. Many APAC countries placed a ban and/or restrictions on the “the new POPs” specifically perfluorohexane sulfonic acid (PFHxS).

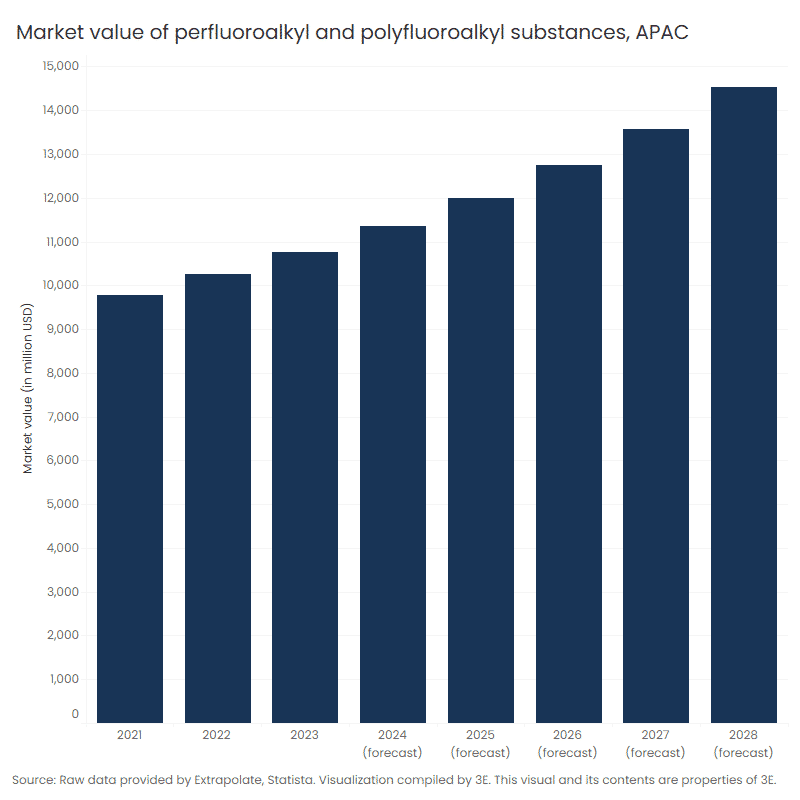

The market value of PFAS in Asia-Pacific countries is expected to rise, but more and more countries are putting stricter regulations on the “forever chemicals.” Specifically, there are increased regulations in cosmetics and some countries are taking further steps to ban PFAS in drinking water.

“More countries are controlling products containing PFAS, not just controlling PFAS itself as industrial chemicals,” said Minglei Gao, regulatory research analyst at 3E.

For example, Taiwan began banning PFAS in cosmetics on 1 January 2025. Japan expanded its ban on products containing perfluorooctanoic acid (PFOA) to include PFOA-related compounds and isomers in products such as fabrics, repellents, fire extinguishers, and floor treatments on 10 January 2025. In September 2025, Australia will add perfluoro(hexane-1-sulfonic acid) (PFHxS), perfluoro(octane-1-sulfonic acid) (PFOS), and PFOA to its List of Chemicals with High Hazards, which could introduce further obligations and requirements for companies who manufacture or import these chemicals.

“These developments highlight a growing regional commitment to addressing the risks associated with PFAS,” Utiskul said. “To ensure compliance and maintain market access, businesses should prepare for tighter controls and align their practices with evolving regulations.”

In addition to classifying PFAS as hazardous chemicals and requiring permits under the traditional chemicals management scheme, several countries are adopting or planning to implement progressive measures on PFAS to align with regulatory trends set by the U.S. and EU.

For instance, following the EU's proposal, New Zealand will ban PFAS in cosmetics starting January 2027. Similarly, the Association of Southeast Asian Nations (ASEAN) recently added perfluoroheptanoic acid (PFHpA) to the banned cosmetic list under the ASEAN Cosmetic Directive. Additionally, concerns over PFAS contamination in drinking water are increasing. Korea already regulates PFOA, PFOS, and even PFHxS in drinking water. Taiwan plans to enforce stricter limits on the maximum PFAS content in drinking water by July 2027. Similarly, Japan restricts PFAS in drinking water and monitors their presence.

GHS Adoption

Many countries are gearing up to update their GHS rules in 2025. GHS standardizes hazard testing criteria and the classification and labeling of hazardous chemicals, primarily in accordance with the UN's GHS system.

An update of China's GHS is expected in 2025, which means China will officially move from GHS Rev. 4 to GHS Rev. 8 and will gradually amend all its GHS classification standards, known as GB 30000, to align with GHS Rev. 8. In addition, China is also revising its GHS labeling standard GB 15258. Once finalized and adopted, the revision would require companies to add a product-based QR code on their GHS labels.

Malaysia may also finalize GHS rules per the proposed GHS Rev. 8 adoption this year, and New Zealand will require compliance with the EPA's April 2021 updated Classification, Labeling, Safety Data Sheets, and Packaging Notices according to GHS Rev. 7 by May 2025.

Additionally, Singapore will mandate compliance with the GHS Rev. 7 starting in February of 2025, requiring chemical suppliers to update their SDS and labels for their hazardous chemical products accordingly.

Japan was expected to adopt GHS Rev. 9 in 2024, but it didn't happen. The new revision date is unknown but could potentially occur in 2025.

—————-

Editor's Note: With our 2025 Outlook series of articles, we examine the regulations, trends, challenges, and achievements shaping our companies, our industries, and our world in 2025 and beyond.

Insights straight to your inbox

Sign Up NowReporter

Sheridan Wood

Sheridan Wood is 3E's Industry Reporter. She has reported on local, state, and national news for public radio stations KACU, The Texas Standard, and National Public Radio. She has won regional and national reporting awards from the Society of Professional Journalists.

Related Resources

News

EU Omnibus Packages Part 5: Omnibus V – Simplifying EU Defense Regulation

News

EU Omnibus Packages Part 4: Omnibus IV — Product Regulation, Simplification, and Compliance

News

Athletes Disqualified at 2026 Winter Olympics Over PFAS

News

EU Omnibus Packages Part 3: Simplifying EU Agricultural Regulation