Related

EU Omnibus Packages Part 5: Omnibus V – Simplifying EU Defense Regulation

EU Omnibus Packages Part 4: Omnibus IV — Product Regulation, Simplification, and Compliance

Athletes Disqualified at 2026 Winter Olympics Over PFAS

EU Omnibus Packages Part 3: Simplifying EU Agricultural Regulation

The UK's chemical industry has been described as being in a crisis by industry leaders across the sector. Primary concerns are weakening demand, labor costs, and most of all, sky-high energy prices. A recent survey by the Chemical Industries Association (CIA), the UK's national association for chemical and pharmaceutical manufacturers, showed that 60% of chemical businesses reported falling sales while 20% reported no growth. It also found that in 2024, the UK chemical output reached its lowest level in more than a decade.

Steve Elliott has been at the CIA since 1997 and has served as the CEO for nearly 20 years, following 15 years at the Department of Trade and Industry. He is actively involved in various organizations, including the Control of Major Accident Hazards Strategic Forum and Building a Safer Future Ltd. Additionally, he sits on the board of the Institute for Employment Studies (IES), an employee relations think-tank; is a trustee of the chemical industry's training body, CogentSkills; and chairs the European Chemical Industry Council (CEFIC) Communications Network.

3E's Industry Reporter Sheridan Wood sat down with Elliott to discuss concerns facing the UK's chemical industry and the policy potentials that could contribute to its rebound.

This interview has been edited for clarity and length.

The UK chemical industry has been described as being in crisis. What is causing this outlook and how dire is it?

Since January 2021, our production volume has fallen by nearly 40%. A couple of pieces of context there. January 2021 was a real high point in terms of production because we, like American Chemistry Council members and others around the world, were responding to COVID and [the] solutions needed. We were one of the industries that kept running throughout COVID. From January 2021 to the back end of last year, [there was] a 38% fall in production. The biggest fall was in two years, '22 and '23, and in '24 still a decline, but it’s been a more gradual decline since a real falloff in '22.

Our message [to politicians has been]: We might stabilize this year; it might not get any worse. But if it's going to improve, the second half of this year at the earliest is when we think that might happen.

The falloff is not a Brexit consequence. Brexit to some degree might have had some impact because the EU collectively is our largest, most important marketplace. But the message is broader than “it's a Brexit phenomenon” in terms of the falloff.

It's been the cost of energy. It's been the uncertainty and short-termism of policy adopted in the carbon reduction space by our government and allied to that some other regulatory stand-still stuff [with] Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) being a good example.

And on top of that, we've had suppressed demand for nylon for over two years now, which is quite unusual in our industry. [Cyclically things usually] pick up and you have all your destocking, then people restock, quite often to a more ambitious degree. But none of that has really happened yet.

This suppressed demand has run on longer than many people might have expected. And at the same time, Chinese excess capacity is actually coming to Europe, including the UK. [That's] partly because Chinese domestic demand has fallen and partly because, and I think this will be a worry for us looking forward, the U.S. market might be less attractive with tariffs on board for Chinese product that it might go elsewhere.

Where are the specific gaps in demand, and what is causing them?

The strongest contraction is in petrochemicals and in agrichemicals. They've been the worst performing, and they are typically in that high-volume, low-margin, globally exposed commodity area. The weak demand has really had two main causes. One is that fierce competition from third-country markets, and our high energy prices have pushed up our production costs in the UK and the EU whilst the U.S., China, and the Gulf countries can still produce lower reduction costs and sell at lower prices. So, the demand has shifted away from the UK and EU producers.

And the second cause of the weak industrial production in the UK and the EU is the energy crisis has strongly impacted European industrial sectors, which are our main consumers. Until we get the recovery of that wider industrial sector demand, the demand for chemicals will remain weak.

And if there's anything else, it's that divergence in the playing field compared to the U.S., following the announcement of the Inflation Reduction Act (IRA). Now, [it will be] interesting to see what happens to IRA and all those incentives, because if I listen to the president now, that's about to be rolled back big time, but we'll see.

So, it's a bunch of reasons that I think explain the ongoing falling demand. We will hopefully mirror our UK economic growth, the generally wider GDP growth anticipation from the year in the UK (which is maybe around 0.81%, something like that). We might get to that this year for chemicals. But again, that's having fallen so much over the past three years.

How does the energy price in the UK compare to Europe, and why is it so much higher in the UK?

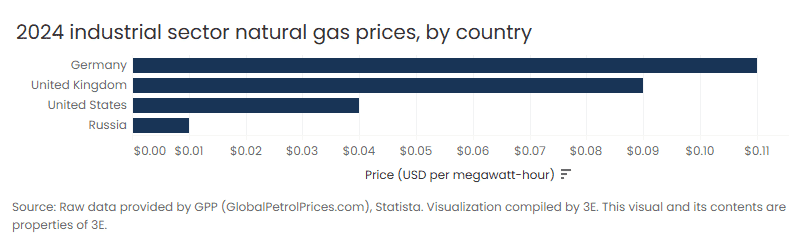

We are not a million miles away from European-wide prices and haven't been on gas. That's partly been our access to our own sources, gas storage, and the fact that we are less exposed to Russian gas supply. The gas piece has seen a smaller differential, but as far as the electricity price in Europe, we have seen a differential.

I think that's primarily because historically, continental European consumers, domestic consumers, have paid more for their energy bills to help subsidize some of this move to renewables in a way that hasn't happened in the UK. The whole drive towards renewables in the UK, and we were sort of one of the leading lights on that drive, the way that's been paid for has been that the bill landed initially on energy companies, but then energy companies have passed it on to their industrial consumers.

UK industrial electricity prices are the highest, including Europe. That's not us saying it, that's the International Energy Agency (IEA) reporting that. UK prices are some four times those in the U.S., but they are two, nearly three times those of Korea, and they're 46% higher than the IEA medium. But given that UK gas prices are below the IEA medium, and those in France and Germany, it's not the gas prices that are driving high electricity prices, but it's the policy cost element piece.

The irony is that this is being felt by the industry that's going to drive the net zero agenda in terms of the products and solutions that enable ever lighter, more fuel-efficient planes, cars, etc.

Energy's a big differential, and then the carbon reduction ambition also is one that we face a serious challenge on. If you look at our CO2 emissions reduction performance as the UK, it's very strong, but a lot of that increasingly has been driven by what we would say is deindustrialization rather than decarbonization. Basically, plants are closed, and we've offshored the emissions, but we're still importing the product from other jurisdictions. Is that truly decarbonization? Of course it's not. We have a number of things in place in the UK to encourage energy efficiency and some of those vehicles are quite helpful. But the whole trajectory around CO2 emissions reduction is driven by our emissions trading scheme, and businesses [have] a certain number of free allowances, which, if they're not making, they can trade to meet compliance.

The timeline for a more severe restriction in those allowances is 1) not very visible [in] the short term and 2) too tight. I think at the moment we only see it head to 2027, in terms of what that allowance cap and trajectory is. And when you're talking to industries that typically have five, 10, 15-year investment cycles, the ability to only see a couple of years ahead is just not helpful.

You will see us increasingly talk about ideally a global carbon tax. I'm not sure, given very recent political developments in [the U.S.] that can happen.

What we are looking to do, wherever possible, is align on some of those climate change-addressing instruments with the EU. Can our UK and the EU emissions trading schemes be aligned better? And when it comes to carbon border adjustment measures and tackling that imported carbon piece, the EU is already progressing ahead and has its scope. We will be following those in some respects over a slightly different timeline, but again, can we start to align better there? But all of this is coming at a time when we have a very aggressive Trump agenda around “drill baby drill,” etc., and that's opposite a European-wide investment climate that is unattractive.

Talk to me more about the policy and regulatory issues that are contributing to the industry's decline. What specific policies are being referred to, and what does the UK government need to do to promote success for industry?

Some of the [things we think we need based on scenario-based research] are more politically challenging than others. The one that is most politically challenging is if we're paying four times the price for electricity than a U.S. competitor is paying, what do we do about that? And if you start to try and alleviate the cost of energy in the UK, someone else has to pay.

So, the options are the government sticks the excess cost on to you and me as the domestic consumer. It'd be a very brave government that did it. But the issue is, UK businesses are paying the highest power prices in the world, but us as domestic consumers are paying something like the fifth or sixth highest prices in the world already. So, do you really want to load more cost on the voter? That's a tall order.

The alternative is to shift the cost away from electricity to gas. And unfortunately, we still have too many businesses that are dependent upon gas. The ability to move from gas to renewables is determined, amongst other things, by connectivity to the national grid. All this stuff takes time and is very expensive. So that particular piece of relief around the cost of energy, given it is four times different than the states, is the most politically difficult of all decisions to make.

But something needs to give. It's just impossible to compete on that cost of energy, particularly when the cost of energy can, for some businesses, account for 50% plus of their operating cost. We do need relief on power prices, and there are some things for some of the energy-intensive companies that the government has started to do. We want to see more of that. It's things like relief on network charges. There are already some compensatory measures in place for the very largest users of energy to help them transition. We want those retained and we want them enhanced.

But we think there's a political choice to be made over the overall cost of energy. The government has to weigh up: Is it better to irritate the voter now or is the consequence of not doing that that you lose more factories, more highly skilled jobs, and ultimately more votes in parts of the country in four- or five-years' time that you really need?

What needs to happen for the industry to recover?

It's been a challenging time for our industry, and we need help. The help we require is an investment in the future of the chemical industry and the wider economy because we are macroeconomically important. We underpin critical national infrastructure. We underpin the rest of manufacturing. McKenzie, who did this work years back, [said] about 96% of anything made is dependent on the chemical industry. And that's as true for the identified growth sectors in this country, which include automotive, aerospace, life sciences, and the whole clean energy, clean tech, net zero transition piece as well. That all requires chemistry and chemicals.

We're saying to the government: We need some help, particularly over the next few years, to stem the flow of closures and strategic reviews and the like. But the investment will lead to more of all those things, which would give them, we hope, better political prospects, would give us better commercial prospects, and will give the wider economy a better contribution to the growth agenda. And the things that are holding us back most from doing all of that are 1) the cost of energy, 2) the piece around carbon, and 3) schools and labor. Some of that is within our control and making ourselves more attractive as an employer, but the broader regulatory piece [is where we need help].

———————–

Editor's Note: 3E is expanding news coverage to provide customers with insights into topics that enable a safer, more sustainable world by protecting people, safeguarding products, and helping businesses grow. Industry News highlights insights, trends, and financial results from a global perspective, and features analysis and interviews from industry influencers and leaders.

About the Contributors:

Adnan Malik is a Production Specialist and Graphic Designer on 3E's News team. With nearly a decade of experience, he specializes in various design solutions. He holds a Diploma in Information Technology, which complements his extensive expertise in various fields and industries.

Dolan Harrington is a Data Journalist at 3E. His analytics career has spanned organizations including Delta Air Lines, Pendo (a unicorn product analytics startup), and S&P Global. He has a master's degree in business analytics from William & Mary.

Insights straight to your inbox

Sign Up NowRelated Resources

News

EU Omnibus Packages Part 5: Omnibus V – Simplifying EU Defense Regulation

News

EU Omnibus Packages Part 4: Omnibus IV — Product Regulation, Simplification, and Compliance

News

Athletes Disqualified at 2026 Winter Olympics Over PFAS

News

EU Omnibus Packages Part 3: Simplifying EU Agricultural Regulation