Related

EU Omnibus Packages Part 5: Omnibus V – Simplifying EU Defense Regulation

EU Omnibus Packages Part 4: Omnibus IV — Product Regulation, Simplification, and Compliance

Athletes Disqualified at 2026 Winter Olympics Over PFAS

EU Omnibus Packages Part 3: Simplifying EU Agricultural Regulation

Since the pandemic, chemical companies are continuing to respond to a consistently turbulent market. Although the U.S. economy is looking more favorable going into 2025 and demand for chemicals is projected to improve, the only thing chemical companies can really be sure of is the continued need to navigate an unpredictable market.

“Every company in the chemical industry will likely be affected by issues related to macroeconomic and geopolitical uncertainties, changing markets, advanced technologies, and new ecosystems,” said David Yankovitz, principal at Deloitte Consulting LLP in a webinar. “It's clear companies need strategies that will allow them to both weather this uncertainty but also position themselves for long-term competitiveness and growth in a high-tech, low carbon future.”

Going into 2025, Yankovitz outlined five key trends experts are watching in 2025: cost efficiency, end markets, innovation, sustainability, and supply chain. Before we talk trends for 2025 and beyond, let’s take a look at the current economic environment for the chemical industry and how that will impact its future.

Macroeconomic Environment

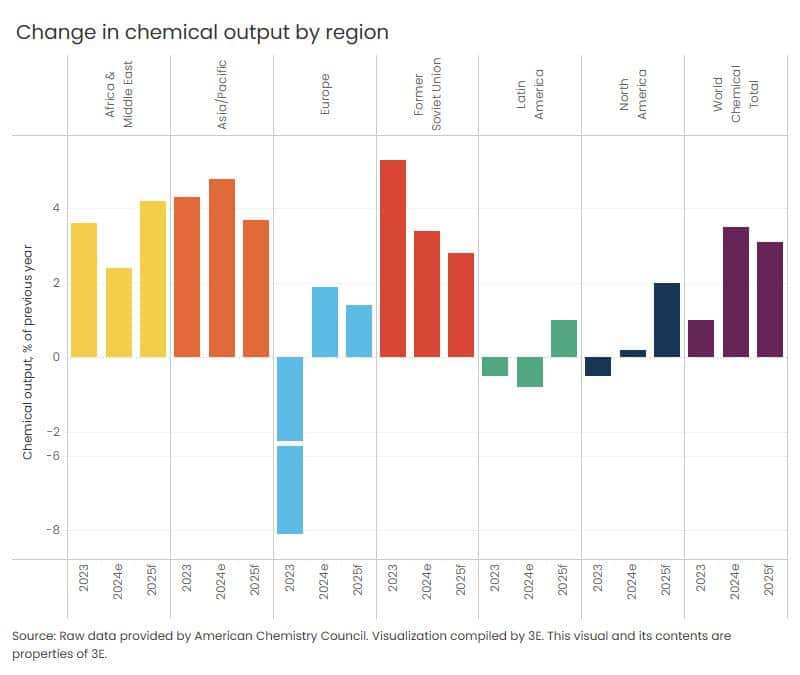

Martha Moore, chief economist at the American Chemistry Council (ACC), said the U.S. economy was “reasonably healthy” at the end of 2024. Global industrial production grew moderately in the last year with a 1.3% increase and is expected to continue growing in 2025 with a projected 2.6% increase.

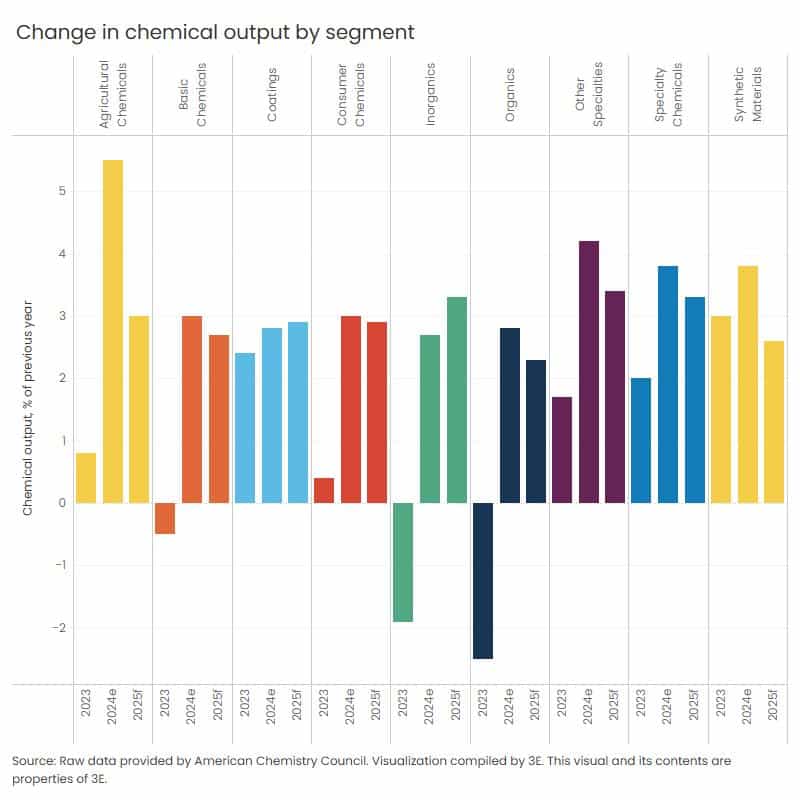

While there is decline projected across most chemical segment output globally, the projected output of U.S. chemical production volumes is expected to increase in most segments, with an estimated 1.9% gain in overall chemical volumes.

“We have good energy fundamentals here in the U.S.,” Moore said. “We've got an energy advantage that persists and capacity expansions in manufacturing.”

Several demand factors will play a role in the macroeconomic environment impacting the chemical industry, including demand around housing and construction, automobiles, and semiconductors:

Housing/construction: With an expected decline down to 1.35 million new homes in 2025 from 1.42 million in 2024, an increase is projected for 2026. Meanwhile, 2025 is expected to be one of the worst years in existing-home sales, which is linked to remodeling activity. “This is a really, really tough time for housing,” Moore said. With an estimated 33,000 pounds of chemistry products in a single-family home, the tough housing market and general construction declines could have implications for some of the chemical industry's construction markets.

Automobiles: After several years of lower-than-average vehicle sales, the ACC expects to see very slight growth in 2025. The ACC reports that there is an average of $4,000 worth of chemistry in every vehicle, and the transition to EVs is promising for the chemical industry.

Semiconductors/high tech: Moore described semiconductors and electrical as a bright spot in the industrial sector, as more than 500 processing chemicals are involved in the production of a single legacy chip. More advanced chips require even more chemicals, with some estimates reaching into the thousands of specialized chemicals.

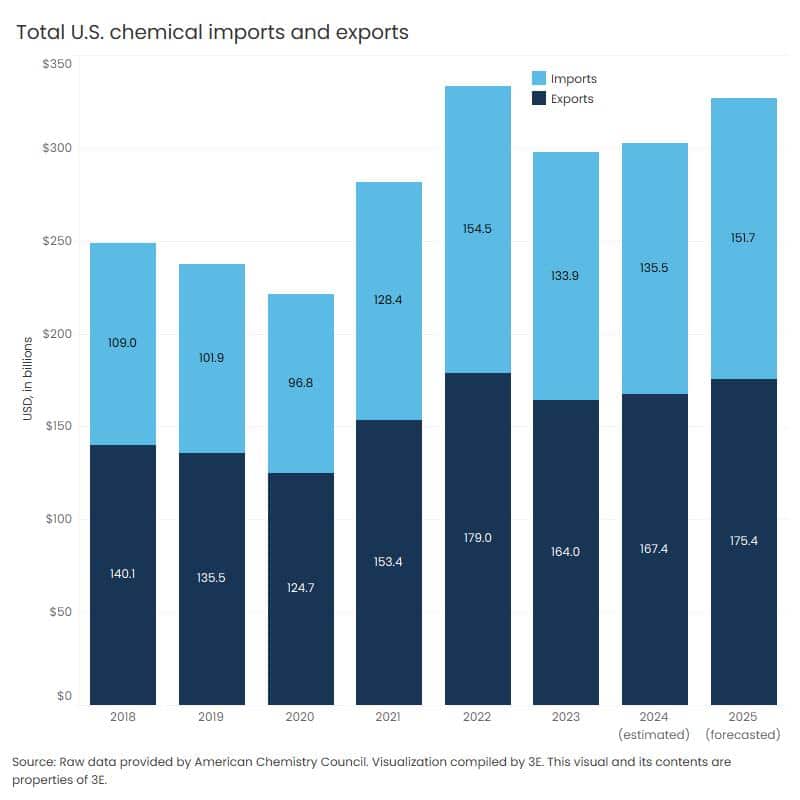

World trade volumes are expected to increase according to data from the ACC, projecting an increase to 3.2% in 2025, up from 2.5% in 2024. With the impending U.S. administration expected to raise tariffs and the possibility of other nations retaliating by imposing their own tariffs, the macroeconomic environment as a whole could face significant complications.

“If tariffs are raised to the levels that have been talked about, that would be troubling to the U.S. economy and to chemical demand,” said Moore. “The chemical industry is exposed on both the import and export sides.”

Although global industrial growth and the U.S. economy are forecast to trend in a favorable direction, the chemical industry is “not out of the woods yet,” according to Yankovitz. He said the macroeconomic environment remains unpredictable, and in the last quarter, several companies reported earnings misses, and some Q4 projections are looking “choppy at best.”

“Looking ahead, there's no doubt that the uncertainty will continue,” Yankovitz said. “How a company responds will be important to maintain performance,” he noted, adding that for some companies, their very survival might be in jeopardy.

Cost Efficiency

With the uncertainty in the market and a turbulent macroeconomic environment over the last few years, more and more companies have adopted cost efficiency programs, a trend expected to continue in 2025. Overcapacity issues are affecting different production and regional sectors, driving companies to rethink cost efficiency. Inflation and high feedstock and energy prices are putting pressure on European companies; low demand from China and a volatile liquified natural gas (LNG) market are impacting Asia-Pacific companies; and even in the U.S. and Middle East, where energy and feedstock prices are lower, companies are still adopting cost-cutting measures to make up for lacking margins.

“In the petrochemical sector specifically, excess production capacity in combination with lower-than-expected demand has contributed to lower operating rates,” said Robert Kumpf, managing director of Deloitte Consulting LLP during the webinar. “That's been a theme.”

Mergers and acquisitions have been an opportunity to facilitate cost efficiency for companies in recent years, and that will likely continue, particularly if interest rates continue to rise. Additionally, an increase in operations consolidation and closures, specifically in Europe, is trending as a cost-efficiency measure and is expected to continue in 2025.

End Markets

After slow economic growth through 2023 and 2024, 2025 is promising an increase in global chemical demand.

“Growth is expected to trickle back to the chemical markets in 2025, but this growth will likely be uneven across products and specific applications,” Kumpf said. “In response to this, many chemical companies are focusing on driving efficiency in their core businesses while simultaneously investing in what they see as high growth areas and always enhanced customer centricity.”

The primary, high-growth markets companies are shifting to focus on the demand for advanced technology and clean energy:

High tech: The rising demand for EVs and other car electronics and the AI-fueled demand for data centers are creating a strong market for specialty chemicals and gases that go into semiconductor manufacturing, which is good news for the chemical industry. The chemical industry is also bringing solutions to lightweight vehicles as EVs take over the roads, and the significant market for solutions in making EV batteries lighter presents the industry with opportunity for innovation.

Clean energy: Chemistry is essential to the clean energy transition. Not only does chemistry bring solutions for battery storage and clean hydrogen, but it is also required for the industrial materials that support the construction of clean manufacturing facilities themselves. We can expect to see growth in fabricated metals, construction supplies, and iron and steel products as investment in green energy continues.

Companies are also fostering stronger customer relationships and coming up with solutions specifically tailored to meet customer needs.

Innovation

Continued innovation is essential for companies looking to continue growing in today's dynamic and unpredictable landscape. In addition, as Yankovitz said, this innovation will be required to improve operational efficiencies and enhance end-product performance while meeting end-market needs and sustainability goals.

Because of the need for innovation, companies have and are expected to continue investing in capital expenditure (CapEx) and research and development (R&D). Even in 2023 when revenues dropped, CapEx and R&D investments grew.

Yankovitz said R&D is a particularly important investment for companies in solutions spaces as they aim to provide new and more tailored solutions to solve customer problems. Even though interest rates slowed CapEx in 2024, that is expected to pick up in the new year along with R&D.

“Success in the solutions space requires clarity and understanding how to bring innovative ideas to meet market needs,” he said.

Yankovitz said companies are dividing innovation across three dimensions: product, which focuses on feedstock substitution, improved formulations, additives, and end-market applications; process, which focuses on efficiency through digital automation and sustainable methods; and ecosystem, which collaborates with industry, research institutions, and startups to develop circular economy solutions.

“No other industry [is better] positioned to meet the future material needs in areas such as mobility, building materials, personalized health, packaging, and the energy transition,” Yankovitz said. “These all require new and advanced materials and systems developed by chemical and material science companies, requiring an ever-shorter innovation cycle.”

Sustainability

The chemical industry is continuing to make progress in emissions reporting, with reporting rates rising by 46% between 2013 and 2022 in scope 1 and 2 reporting and 83% in scope 3 reporting. Yankovitz highlighted three areas influencing decarbonization for the chemical industry: access to clean energy, policy levers, and the ability to capture value across ecosystems.

Access to clean energy remains limited. Sourcing is challenging, and evidence suggests that renewable energy would need to increase threefold from 2021 to 2030 to meet high energy demands. However, this estimate could increase significantly, specifically with the growing popularity of AI. Although that is good news for the chemical industry, as chemistry is necessary for progressing renewable energy innovation, implementing renewable energy for chemical companies themselves will continue to be a challenge. Some companies have invested in onsite clean energy facilities, but the cost that comes with that is not a feasible option for every company.

Policy levers globally will continue to influence investment in sustainable products. Permitting processes are sometimes a barrier for companies working to green their processes, and the ever-changing regulatory landscape makes it difficult for companies to keep up with requirements and lengthy permitting processes.

Capturing value across markets is challenging for the chemical industry. Yankovitz said companies upstream that need to make investments to reduce emissions struggle to get the return on investment needed by tracking products through the supply chain. Innovative strategies, including carbon footprint assessments, are essential to tracking environmental impact across the supply chain.

“In order to maintain or accelerate the momentum towards sustainability, companies will need to continue navigating these three factors in 2025,” Yankovitz said.

Supply Chain Resiliency

In the last few years, building supply chain resiliency has become more and more of a focal point for companies looking to future-proof their businesses. COVID, intensifying weather due to climate change, and geopolitical conflicts over the past several years have emphasized the need for flexibility and agility in supply chains in a globalized, interconnected world. Global chemical trade has grown over the past six years and is expected to continue doing so. While China and the U.S. are leading in chemical exports, India, Southeast Asia, and the Middle East are emerging as major producers.

While global trade is beneficial and essential in many markets, it also creates vulnerabilities for companies whose supply is limited to certain regions. Geopolitical disruptions, climate events, and regional policy changes are making supply chain agility, visibility, and flexibility more critical than ever.

For example, we've seen Europe forced to rethink sourcing strategies as the Russo-Ukrainian War has continued to escalate, reducing Europe's natural gas supply, much of which was originally sourced from Russia. Additionally, drought conditions have reduced traffic capacity in the Panama Canal, affecting trade routes and shipping costs. Regional shifts in supply and demand are influencing trade flows, evident in China's decreased consumer demand for automotives and a weak housing market, affecting the global chemical industry at large.

“As we proceed through 2025, enhancing supply chain flexibility and agility could help companies weather these changes and even capitalize on growth opportunities,” Kumpf said.

Along with the challenges, awareness of the global supply chain can open opportunity. Regionalization incentives are shifting global markets, evident for example in the case of battery manufacturing shifting from China to the U.S. Additionally, innovative tools are being developed to make supply chain tracking and analysis easier. AI and analytics tools could improve demand forecasting, real-time tracking, and decision-making. Some companies are also decentralizing and diversifying their supply chains to mitigate risk. Other companies are participating in ever-increasing collaboration and joint planning with suppliers and customers to foster transparency, reduce uncertainty, and enhance overall performance and security.

“By leveraging these strategies, chemical companies can better navigate regional market dynamics and thrive in a rapidly changing environment,” Kumpf said.

Signposts to Watch in 2025

Along with the trends in cost efficiency, innovation, supply chain, end markets, and sustainability, Kumpf highlighted four signposts that companies and industry leaders need to keep an eye on throughout the next year, including macroeconomic conditions, policy and the regulatory landscape, global risk, and portfolio transformation.

Macroeconomic conditions: Global GDP, inflation, and interest rates will continue to influence production rates, even with the projected moderate growth. Ultimately, even though growth is projected in 2025, economic conditions remain uncertain, and many companies will likely continue to focus on high-growth regions and cost-reduction plans in preparation for that uncertainty.

Policy and regulatory landscape: Climate and environmental policies around the globe have been changing for the past few years, and that is expected to continue in 2025. This was true even before the 2024 U.S. presidential election, which will undoubtedly bring massive changes to the U.S. regulatory environment during President Donald Trump's administration. Companies will need to stay agile to adapt to evolving regional policies on topics such as emissions, tariffs, and investment incentives.

Global risk: Geopolitical tension and climate events will continue to impact supply chains and pricing for the foreseeable future. “Companies should continue to invest in supply chain flexibility and agility to be able to quickly adapt to these disruptions since we know they are coming,” Kumpf said.

Portfolio transformation: In response to the uncertainty of the market, companies will likely continue to rationalize their portfolios to reflect the changing market and economic conditions, and there is expected to be more mergers and acquisitions and joint partnerships as companies search for ways to strengthen their portfolios.

————————————

Editor's Note: 3E is expanding news coverage to provide customers with insights into topics that enable a safer, more sustainable world by protecting people, safeguarding products, and helping businesses grow. Deep Dive articles, produced by reporters, feature interviews with subject matter experts and influencers as well as exclusive analysis provided by 3E researchers and consultants.

About the Contributor: Dolan Harrington is a Data Journalist at 3E. His analytics career has spanned organizations including Delta Air Lines, Pendo (a unicorn product analytics startup), and S&P Global. He has a master's degree in business analytics from William & Mary.

Insights straight to your inbox

Sign Up NowReporter

Sheridan Wood

Sheridan Wood is 3E's Industry Reporter. She has reported on local, state, and national news for public radio stations KACU, The Texas Standard, and National Public Radio. She has won regional and national reporting awards from the Society of Professional Journalists.

Related Resources

News

EU Omnibus Packages Part 5: Omnibus V – Simplifying EU Defense Regulation

News

EU Omnibus Packages Part 4: Omnibus IV — Product Regulation, Simplification, and Compliance

News

Athletes Disqualified at 2026 Winter Olympics Over PFAS

News

EU Omnibus Packages Part 3: Simplifying EU Agricultural Regulation